When scanning the market for dividend stocks, you’re sure to notice companies with high yields. But it’s arguably more impressive when companies pay and raise their dividends every year no matter what the economy is doing. Consistent dividend raises often coincide with financial health and steady earnings growth.

Emerson Electric (NYSE: EMR), NextEra Energy (NYSE: NEE), and Clorox (NYSE: CLX) don’t have mind-numbingly high yields. But all three companies are well on their way to extending their streak of dividend raises for decades to come.

Here’s why all three dividend stocks are worth buying now.

Repositioning the company in growth markets will ensure more dividend growth in the future

Lee Samaha (Emerson Electric): After adjusting for stock splits, Emerson Electric has increased its dividend every year since 1956, and its growth potential ensures plenty more to come.

The industrial company has been transforming over the last few years as management steers it toward a future focused on automation and related markets such as test and measurement, industrial software, and smart grid solutions.

The idea is to reposition the company in growth markets that will benefit from long-term megatrends such as labor automation, the electrification of everything, reshoring manufacturing (which implies increased demand for automation and smart factories), and the digital revolution in manufacturing and processing.

Having sold the remaining vestiges of its climate technologies business, acquired automated test and measurement company NI, and closed a transaction resulting in a 55% stake in industrial software company Aspen Technology (NASDAQ: AZPN), management has positioned the company for future growth.

That growth will likely kick in after some of its end markets recover from a slowdown in 2024. For example, investment in its factory automation and test and measurement business is currently weak due to a downturn in the economy and a pullback in investment from industrial customers in production capability (factory automation) and research and development (test and measurement).

A lower-interest-rate environment will help in 2025, and the underlying long-term secular trends discussed above will continue, enabling Emerson Electric to generate the 4% to 7% organic revenue growth management expects to achieve through the ups and downs of the economic cycle.

With three decades of dividend growth under its belt, NextEra Energy plans on powering its payout even higher

Scott Levine (NextEra Energy): A lesson you may remember learning at the beginning of your investing journey is that previous performances don’t guarantee future results. But looking at previous performances can still be useful.

Take utility stock NextEra Energy, for instance. The company has increased its dividend for 30 consecutive years, and while it’s not guaranteed to continue doing so for the next 30 years, that’s certainly an auspicious sign. And that’s just for starters. For those looking to supplement their passive income streams, NextEra Energy stock — along with its 2.5% forward-yielding dividend — looks like an attractive option right now.

Conservative investors won’t find only the past 20 years of dividend increases compelling; the steady earnings and cash flow growth have supported the dividend. From 2003 to 2023, NextEra Energy has boosted its dividend at a 10% compound annual growth rate (CAGR). Similarly, its adjusted earnings per share (EPS) and operating cash flow increased at CAGRs of 9% and 8%, respectively, during the same period. Lest investors speculate that this means the dividend increases are jeopardizing the company’s financials, consider that the company has averaged a 60.2% payout ratio over the past 10 years.

All of these accomplishments should give investors confidence that the company will achieve its 2024 adjusted EPS forecast of $3.23 to $3.43, rising at a 6% to 8% CAGR through 2027. Operating cash flow is projected to grow at the same rate or higher. Management expects to raise its dividend at a 10% CAGR per share from $2.06 in 2024 through 2026.

Shares of NextEra Energy have traded at a five-year average operating cash flow multiple of 15.6. They’re now changing hands at a discount: about 12.3 times operating cash flow. This stock seems ripe for the picking.

Clorox has room to run after hitting an all-time high

Daniel Foelber (Clorox): Clorox hit an intraday 52-week high on this week, but there’s still reason to believe the consumer goods stock is worth buying now.

Clorox began paying dividends in 1986. It has raised its dividend every year since then. Despite the run-up in the stock price, Clorox still yields 2.9%, which is more than the 2.6% average yield in the consumer staples sector.

Clorox has rocketed higher since undergoing a steep sell-off this summer, with the stock now up 24% in just three months. That’s a big move for a stodgy company like Clorox.

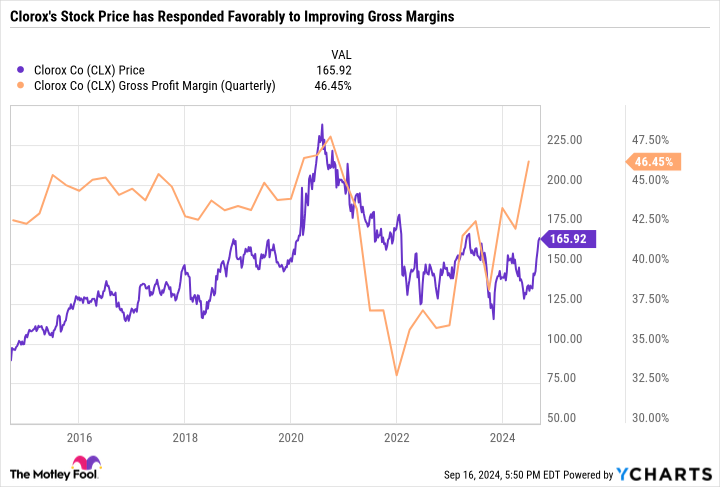

The rebound is likely due to improving gross margins. Clorox’s margins initially surged during the peak of the COVID-19 pandemic, only to nosedive after Clorox bet too big on consumer demand trends toward cleaning products and hygiene. The following chart shows that Clorox’s stock price has returned to around its pre-pandemic high, and so have gross margins.

It took a few years and multiple operational blunders, but Clorox has finally found its footing. Management expects gross margins to tick up another 100 basis points in fiscal 2025. It also expects $6.55 to $6.80 in adjusted EPS. At the midpoint, that would be an 8% increase from fiscal 2024 and would give Clorox a forward price-to-earnings ratio of 24.9 on an adjusted basis. That’s not dirt cheap, but it’s reasonable if Clorox can continue high-single-digit earnings growth.

Clorox is known for its flagship cleaning products, but the company owns a variety of brands across categories including cleaning, home care, wellness, and lifestyle. You may be surprised to learn that Clorox owns Brita, Burt’s Bees, Glad, Hidden Valley, Kingsford, Pine-Sol, and dozens of other brands.

When Clorox is at the top of its game, it is a diversified conglomerate with high-margin products that lead or are close to leading their categories. Clorox hasn’t been at that level for some time, but it’s getting there again, making now a good time to scoop up shares of this high-quality dividend stock.

Should you invest $1,000 in Emerson Electric right now?

Before you buy stock in Emerson Electric, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Emerson Electric wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $708,348!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

See the 10 stocks »

*Stock Advisor returns as of September 16, 2024

Daniel Foelber has no position in any of the stocks mentioned. Lee Samaha has no position in any of the stocks mentioned. Scott Levine has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Emerson Electric and NextEra Energy. The Motley Fool has a disclosure policy.

3 Dividend Stocks to Buy Now That Have Raised Their Payouts for at Least 20 Consecutive Years was originally published by The Motley Fool